The global financial system looks fundamentally different today than it did two decades ago. If the pre-2008 era was characterized by an unbridled expansion of bank balance sheets, the post-2008 era is defined by the meticulous, rigorous, and sometimes restrictive management of capital. As global regulators, led by the Basel Committee on Banking Supervision, implemented waves of reforms—most notably Basel III and the impending "Basel IV" or Basel III Endgame—the core mechanics of finance shifted.

The goal was unambiguous: make the banking system safer, ensure institutions have enough skin in the game to absorb massive losses, and prevent another taxpayer-funded bailout. In this, regulators have largely succeeded. Banks are undeniably better capitalized today. However, risk in the financial system is rarely destroyed; it is merely redistributed.

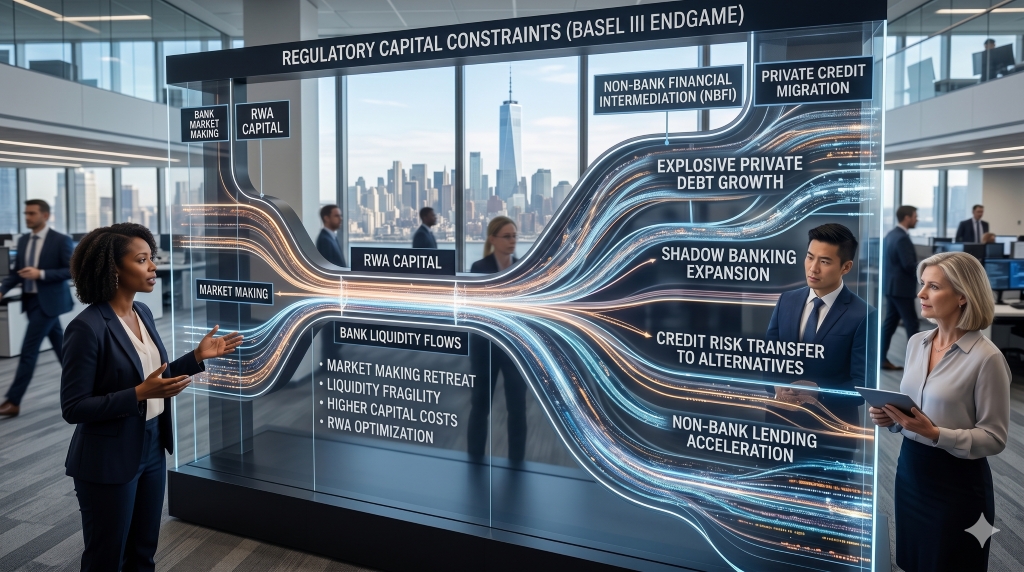

The profound, cascading effect of tying up trillions of dollars in regulatory capital has fundamentally reshaped market behavior. From the withdrawal of major banks from traditional market-making to the explosive rise of shadow banking and private credit, regulatory capital constraints are the invisible hand steering the modern financial ecosystem. Here is a deep dive into how these rules are rewriting the rules of the game.

To understand the behavioral shifts in the market, one must first understand the metrics that keep bank executives awake at night. Post-crisis regulations introduced a web of overlapping requirements that act as speed limits on a bank's ability to take risks or even hold assets.

These constraints treat a bank’s balance sheet like highly expensive real estate. Every square foot—every dollar of exposure—must generate enough return to justify the capital parked against it.

Historically, when financial markets experienced turbulence, large investment banks acted as shock absorbers. If there were more sellers than buyers in the corporate bond or Treasury market, banks would step in, buy the assets, warehouse the risk on their balance sheets, and sell them later when the market calmed down.

Capital constraints, specifically the SLR, have heavily disincentivized this behavior. Because warehousing massive amounts of bonds inflates a bank’s total exposure, it requires them to hold more capital. In an environment where capital is expensive, the return on warehousing low-yield bonds no longer makes economic sense.

The Result: An Agency Model of TradingInstead of acting as principals (trading with their own money), banks increasingly act as agents (simply matching buyers and sellers). When markets are calm, this system works perfectly well, and liquidity appears abundant. But in moments of stress—such as the March 2020 "dash for cash" or the repo market spike in September 2019—liquidity evaporates rapidly. The banks simply do not have the balance sheet space to absorb the influx of selling. Regulators made individual banks safer, but in doing so, they inadvertently made market liquidity more fragile and susceptible to "flash crashes."

If businesses need loans and banks are constrained by capital charges from providing them, who fills the void? The answer is Non-Bank Financial Institutions (NBFIs)—often referred to broadly as "shadow banking."

Over the last decade, we have witnessed a massive migration of credit origination away from traditional commercial banks toward private credit funds, hedge funds, private equity firms, and insurance companies. The global private credit market now exceeds $1.5 trillion and continues to grow at a blistering pace.

Regulatory ArbitrageThis shift is primarily driven by regulatory arbitrage. A private debt fund is not bound by the Basel Committee’s strict capital ratios. They lock up investor capital for 5 to 10 years, meaning they do not face the risk of a "bank run," and therefore do not need to adhere to the LCR or NSFR.

Because they aren't carrying heavy regulatory capital costs, private credit firms can step in to finance leveraged buyouts, mid-market corporate loans, and complex infrastructure projects that banks have abandoned. While this keeps the gears of the economy turning, it worries systemic regulators. Risk has moved from the highly visible, closely monitored balance sheets of banks into the opaque portfolios of private funds.

Faced with stringent capital rules, banks have not simply rolled over; they have become highly sophisticated at "balance sheet optimization." Financial engineering is being deployed not necessarily to take on more risk, but to shed capital requirements.

One of the most profound behavioral shifts is the rise of the Credit Risk Transfer. Let’s say a bank has a billion-dollar portfolio of auto loans or corporate debt. Holding that portfolio requires a massive RWA capital charge. To free up that capital, the bank will enter into a synthetic securitization.

They pay a premium to a third party (often a hedge fund or pension fund) to insure the "first loss" tranche of that loan portfolio. The bank keeps the loans on its books, maintains the client relationships, and collects the interest, but because the risk of default has been transferred to a shadow bank, the regulators allow the bank to drastically reduce its capital requirement. The bank then recycles that freed-up capital into new loans.

In the derivatives market, banks engage in massive "compression" exercises. If Bank A owes Bank B $100, and Bank B owes Bank A $95, they will compress the trade down to a single $5 net exposure. By using advanced third-party optimization algorithms, banks tear up millions of redundant derivative contracts every year, shrinking their gross notional exposure and minimizing their leverage ratio requirements.

Capital constraints have warped traditional pricing mechanisms in financial markets. Because balance sheet space is a finite and costly resource, anything that takes up space gets priced accordingly, leading to persistent market anomalies.

Ultimately, the increased cost of capital is passed down the chain. End-users—whether a pension fund hedging interest rate risk, or an airline hedging fuel costs—often face wider bid-ask spreads and higher transaction costs because the bank providing the service must charge a premium to cover its regulatory overhead.

As we look toward the final implementation of Basel III Endgame and equivalent regional regulations, the trajectory of market behavior is clear. The financial system is bifurcating into two distinct spheres:

Regulatory capital constraints have succeeded in their primary objective: the core banking system is a fortress compared to 2007. But they have also mandated a trade-off. We have traded the localized risk of a major bank failure for the systemic risk of fragile market liquidity, and we have pushed the most complex financial activities into the less-regulated shadows. Understanding this dynamic is no longer just for compliance officers—it is essential for any investor trying to navigate modern financial markets.

For readers looking to explore the mechanics and implications of regulatory capital, the following institutional resources offer deep, authoritative insights:

BA Blocks

Industry Certification Programs:

CFA(Chartered Financial Analyst)

FRM(Financial Risk Manager)

CAIA(Chartered Alternative Investment Analyst)

CMT(Chartered Market Technician)

PRM(Professional Risk Manager)

CQF(Certificate in Quantitative Finance)

Canadian Securities Institute (CSI)

Quant University LLC

· MachineLearning & AI Risk Certificate Program

ProminentIndustry Software Provider Training:

· SimCorp

· Charles River’sEducational Services

Continuing Education Providers:

University of Toronto School of Continuing Studies

TorontoMetropolitan University - The Chang School of Continuing Education

HarvardUniversity Online Courses

Study of Art and its Markets:

Knowledge of Alternative Investment-Art

Disclaimer: This blog is for educational and informational purposes only and should not be construed as financial advice.